– RTB Digital (RTB) is up 300% over the past month on hype and momentum, but no metrics for revenue projections.

– From the analysis of semrush.com, RTB’s crypto-media website, rtb.io, has only received 50 visits per month for the past two months, and there’s a big gap in time between publishing new articles.

– RTB has a history of bad businesses, all of which ended in flames.

– From 2007-2022, the Company operated under the name “Greenbox POS”, a fintech company focused on payment processing. Its revenue remained weak and it was never able to make a profit.

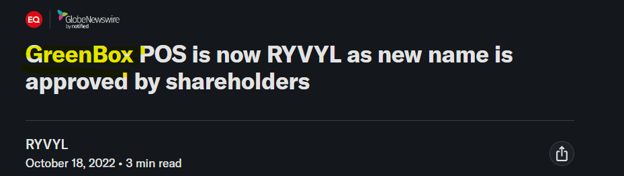

– In 2022, it rebranded itself to RYVYL, which had declining revenue and big losses.

– RYVYL was an allegedly fraudulent company, as its executives settled extensive SEC fraud claims in April 2026.

– After continued declining revenue and large losses, RYVYL announced another rebranding to RTB Digital in October 2025.

– RTB touts that 200 publishers it has a platform that allows media companies to pay their journalists in USDC. But doesn’t quote metrics that show how much revenues does this service actually bring RTB? We think very little.

– There’s lots of potential dilution of RTB, 1.26M shares of warrants and preferred stock, to be converted at about $14 per share.

The Recent 300%+ Uptrend Rally For RTB Digital We Believe Has Now Reversed

RTB is up 300% in the past month, and now boasts a market cap of over $200M. It was trading in the mid $3s in early June, to around $15 today. 2-month chart shown below:

RTB Digital (NASDAQ: RTB), doing business as Roundtable, is being sold to investors as a full-stack AI/DeFi/Web3 enterprise media platform. We believe the reality is it’s a distressed payments shell with legacy fraud baggage that got repackaged into whatever narrative the market wants to pay for. It’s currently a crypto-media website and platform that almost nobody reads. This quarter that narrative is AI, USDC, Web3 and “Coinbase.” Underneath it is a company that lost $17.5M last year, is flagged as a going concern, was past due on its own office rent, and the former executives just settled an SEC fraud action over pretending to have blockchain technology it didn’t have.

RTB is trading at roughly a $200M market cap. We think that number falls apart the moment anyone analyzes the business metrics.

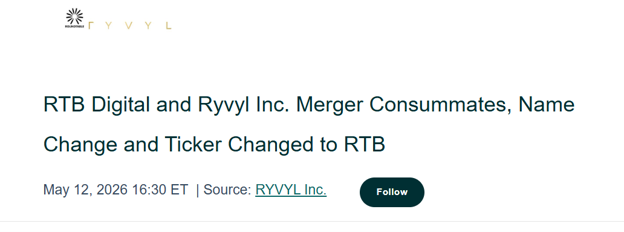

In May 2026, RTB changed its name from RYVVL to RTB Digital Inc due to the consummation of the merger agreement between RYVVL and Roundtable.

The New Story is Heavy on Buzzwords, Light on Disclosed Operating Numbers

RTB describes itself as an AI/DeFi-powered enterprise media platform with real-time USDC settlement, Coinbase wallet/payment support, and a Media Liquidity Pool. The company says nearly 200 publishers are live on the platform.

But the public materials we reviewed do not clearly disclose:

- actual payment volume

- platform revenue

- publisher revenue contribution

- active users

- take rate

- retention

- traffic quality

- audited RTB platform economics

Without those numbers, the valuation rests heavily on narrative.

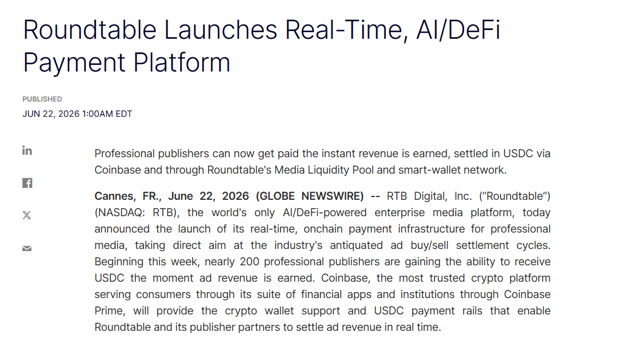

A PR that RTB published on 6/22/26 was aimed at a AI/DeFi payment platform built to serve this roundtable website:

Buzzwords such as AI and DeFi aside, RTB merely announced a payment method that is crypto based instead of cash based, and thought to add the ‘AI’ bit as a complimentary buzzword, even though it has no real context or relevance in this use case. Again, we think this PR will have no economic substance to RTB given that the Roundtable website has thin engagement.

We found the following buzzwords in the PR above:

“The world’s only”

“AI/DeFi-powered enterprise media platform”

“Real-time, onchain payment infrastructure”

“USDC settlement”

“Media Liquidity Pool”

“Smart-wallet network”

“A $200B industry”

Now count the hard numbers. There are none. No audited acquired financials yet. No disclosed revenue scale. No fee numbers or structure. 200 professional publishers are mentioned to be able to receive USDC as payment, but there’s no customer concentration and no publisher list. No pool funding details. No loss economics. No proof Coinbase does anything beyond providing rails.

It’s a very promotional story running well ahead of the hard numbers, and the hard numbers are due around 7/24/26. RTB’s 8-K filed on 5/13/26 states that the financials of RTB Digital from 1/1/24 until 3/31/26 will be filed 71 days after , which would be the date of 7/24/26.

The Valuation Makes No Sense vs. What’s Actually Visible

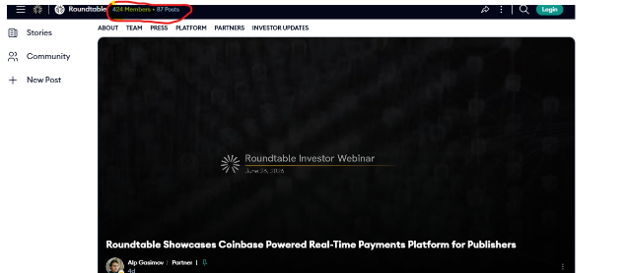

On roughly 13.62M shares and a recent price around $15 to $17, RTB is carrying roughly $200M to $250M of equity value. A number like that only makes sense if Roundtable has real revenue, real publisher adoption, and real platform economics. The visible evidence points the other way. The RTB corporate and investor hub is tiny for something valued like a major media platform, and its own counters don’t even agree with each other. On our checks the main page showed 424 members and 87 posts, the Partner Terms page showed 344 members and 68 posts, and the Partners page later showed 353 members and 68 posts with “No stories found” on the actual Partners tab. When a public company’s own public metadata can’t line up across its own pages, that’s not the footprint of a $200M platform.

“Nearly 200 Publishers” Doesn’t Hold Up When You Look Beneath The Surface

RTB says nearly 200 professional publishers are live, and management keeps repeating that “200 partners” are creating thousands of stories every week. We can’t find a clean public list showing 200 unique, independent, arm’s-length, revenue-generating publisher customers.

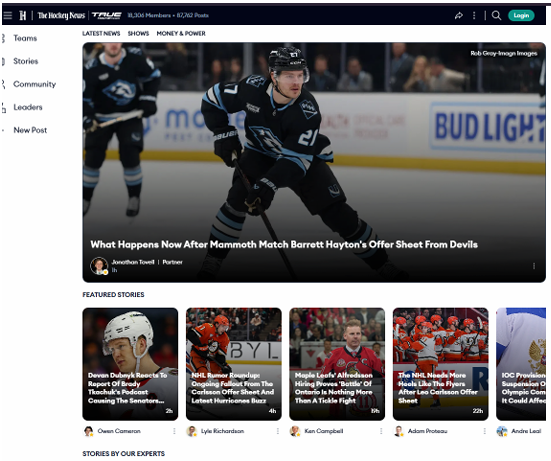

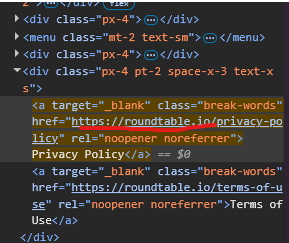

That’s a problem when the whole valuation leans on that number. Roundtable also makes money by packaging up its platform and letting other companies run their sites on it. So we did some internet sleuthing to figure out how big that footprint actually is, and it looks very low. Start with thehockeynews.com, which runs on RTB’s website platform:

Source: thehockeynews.com

The site is basically a clone of rtb.io. If you run inspect element on the page, you find the tags tying it straight back to Roundtable. Shown below:

Source: thehockeynews.com page source

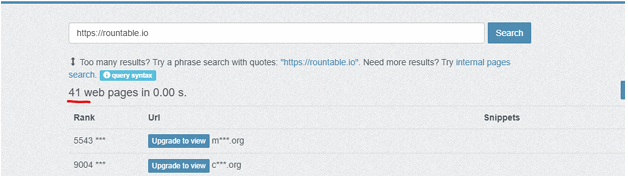

We took that tag and used publicwww.com to estimate how many sites out there actually carry it in their code:

Source: publicwww.com

As shown above, there are only 41 websites using Roundtable’s platform. Nowhere near 200.

And even the count that does exist is built in a way that inflates it. Take the flagship Hockey News example. TheStreet, in an article the company itself provided, says that one deal alone includes 63 applications, made up of 32 NHL team apps, 18 hockey-themed apps, and 13 IIHF apps. That’s one relationship counted many times over. Yahoo should be treated separately too, since management describes it more like a syndication and revenue-share arrangement than a publisher actually running its business on Roundtable. So the issue isn’t that Roundtable does nothing. It does something. The issue is that the market appears to be treating “nearly 200 publishers” as 200 independent customer relationships, when the visible evidence, roughly 40 sites carrying the tag and a headline deal that’s really one relationship stacked into dozens of apps, looks nothing like it. Until RTB shows the actual customer list, the customer revenue, and the economics behind those relationships, the footprint gets nowhere near a $200M valuation.

RTB Digital’s Biggest Announced Deal Is A Related Party

The one commercial “validation” RTB waves around is not a clean arm’s-length demand. RTB’s own Hockey News announcement says W. Graeme Roustan, owner and publisher of The Hockey News, agreed to join Roundtable’s board, and that True Hockey, also owned by Roustan, committed to a long-term advertising and sponsorship deal worth about $15M. TheStreet.com published a promotional article on the deal on 1/6/26.

So this flagship deal is a $15M commitment from a company owned by a man who is simultaneously taking a board seat at Roundtable. We’re not saying it’s fake. We’re saying it’s worth almost nothing as proof of real, independent market demand, because it isn’t independent. That article discloses it was provided by Roundtable, and that Roundtable and its affiliates have a direct financial interest.

RTB Digital Has A History of Bad Businesses, All of Which Ended in Flames

The RYVYL Shitshow

From 2007 to 2022, RTB Digital (RTB) operated under the name ‘Greenbox POS’, a fintech company focused on payment processing.

Then, in October 2022, the company pivoted into being RYVYL, a broader finance company where they specialized in payment infrastructure and banking as a service. PR title shown below:

RYVYL’s legacy business deteriorated sharply before the RTB pivot

RYVYL revenue peaked and then collapsed:

- 2023 revenue: about $65.9M

- 2024 revenue: about $56.0M

- 2025 revenue: about $11.1M

- Q1 2026 revenue: about $2.5M

The company also continued losing money:

- 2023 net loss: about -$53.1M

- 2024 net loss: about -$26.8M

- 2025 net loss: about -$17.5M

This was not a business that rebranded from a position of strength.

RYVYL Executives Settled With The SEC For Extensive Fraud Action

On April 27, 2026 the SEC filed a settled fraud action against RYVYL and its former CEO Fredi Nisan, and former chairman Benzion Errez. In the SEC’s own words, from October 2020 through May 2025 they

“defrauded the investing public by falsely depicting RYVYL… as a cutting edge financial technology company that developed, marketed and sold ‘innovative blockchain-based payment solutions, when in reality RYVYL never processed any transactions through a blockchain… nor did it possess any proprietary blockchain technology,” and “neither sold nor had a functional digital token.”

They also didn’t tell investors until May 2025 that most of their volume was high-risk merchants like cannabis dispensaries. Both settled: permanent antifraud injunctions, five-year officer/director bars, and paid $230,464 each.

The RTB rebrand looks like a narrative reset

RYVYL announced the RTB Digital merger in October 2025. The formal name change to RTB Digital occurred in May 2026, and the ticker changed to RTB on May 13, 2026.

That sequence matters. Investors are not looking at a long-operating public media-infrastructure company. They are looking at a struggling payments company that adopted a new AI/DeFi/media identity after severe revenue deterioration.

RTB’s newest stunt: an online SAAS platform called Roundtable is a sitting duck and as per our research, and won’t amount to anything

In the most recent 10-Q, the company even admits that Roundtable will now be the primary business operating under the RTB umbrella. The 10-Q states:

“Following the merger, RTB’s business will be the primary business of the combined companies, but the Company will continue its current operations, thereafter.”

Therefore, the economic substance of Roundtable affects the terminal value of the company the most.

Roundtable, as per us, will not amount to much economic value, at least not enough to justify a 200 million market cap. The site, rtb.io, has the following layout:

Source: rtb.io

Notice on the top, how the header shows that there are just 424 members with 87 posts. That’s how small the site is. The ‘about’ page of roundtable shows the following:

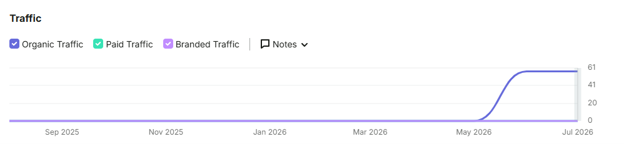

Roundtable is positioning itself as a social media for media companies and while it seems like a respectable vision, Roundtable is failing in its execution. As per SemRush, rtb.io is estimated to receive just about 50 visits a month for the past two months:

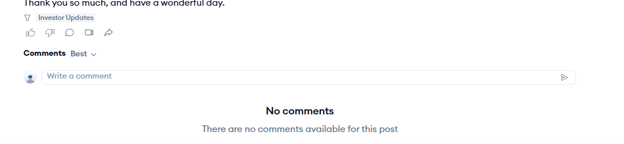

The site and the engagement on the platform itself is so thin, that a post from the team from about 4 days ago has not received any comments:

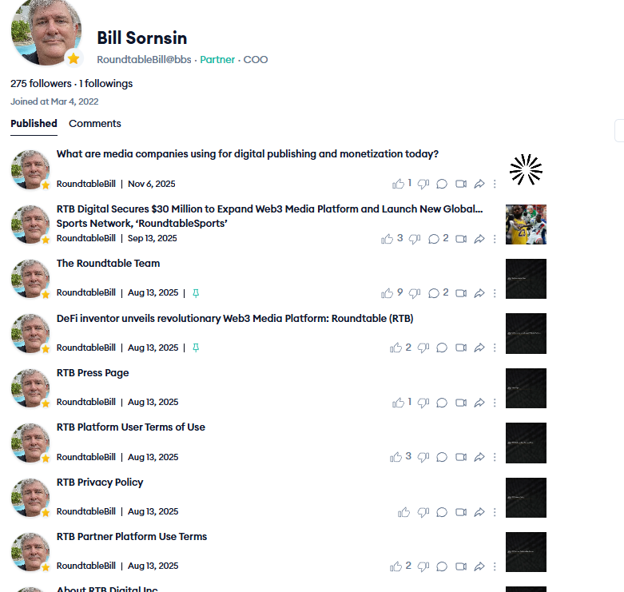

Another example of the lack of engagement on the site is that the second most followed person on the platform, Bill Sornsin, while has posted a lot of content, only has received a maximum of 9 likes in one of this posts:

All in all, we do not think that a company whose main business is Roundtable, or the website shown above with absolutely no engagement, deserves to boast a market cap of $200M.

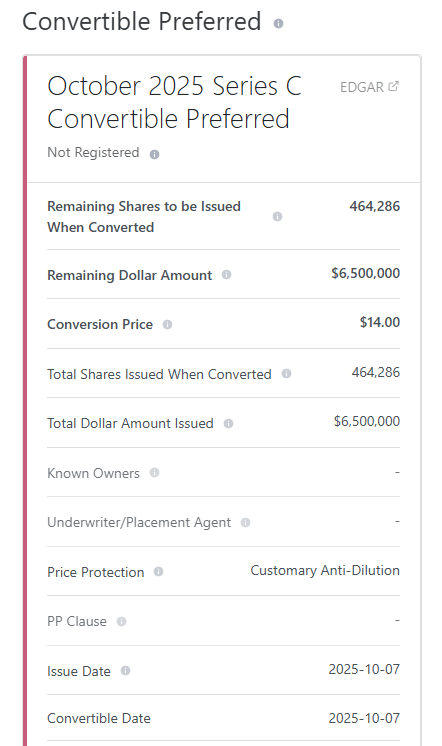

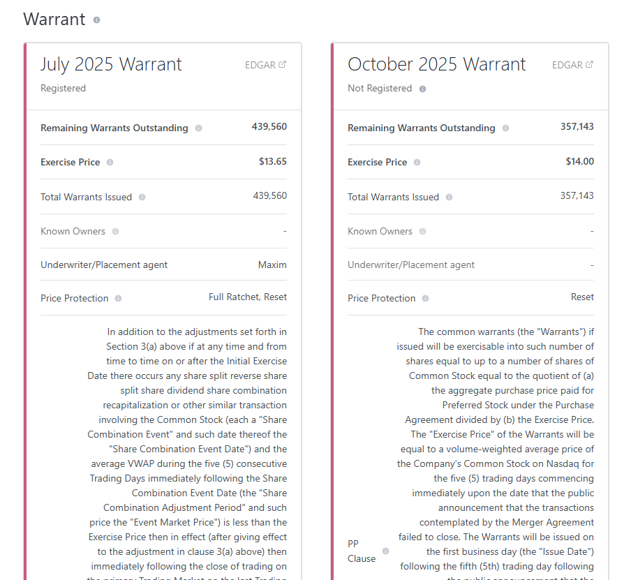

RTB Digital Has Potential Large Dilution At $14 Per Share

There’s about 1.26M shares of RTB, through warrants and preferred stock, that can be added to its float at about a $14 per share conversion price.

Below are shown from dilutiontracker.com RTB data:

Conclusion

RTB appears to be priced as if the market already believes the new AI/DeFi media platform story. We do not think the public evidence supports that confidence yet. The prior RYVYL business suffered a dramatic revenue collapse, the company remained unprofitable, and the RTB pivot introduces a high-concept crypto/media narrative without enough disclosed proof of scale.

Our view: RTB is a high-risk promotional rebrand with valuation downside unless management proves real revenue, real payment volume, and real publisher economics.